Paying Only the Minimum on Your Credit Card: Know the Impact Before You Plan

- Date

- 19 May 2026 14:30

Many people wonder whether paying only the minimum on their credit card will hurt their credit history. When cash flow gets tight, making a partial payment can feel like a manageable way to ease the monthly burden. But before you make that decision, it's worth understanding the full picture - to avoid accumulating debt and to protect your financial standing over the long run.

What Does Paying the Minimum Mean?

Paying the minimum on your credit card means repaying only a portion of the total amount due in that billing cycle. Typically a set percentage of your outstanding balance, such as 8% or 10%, as specified by your financial institution. This keeps your account in good standing and means you're not technically in default. However, the remaining unpaid balance will be subject to interest charges, which become part of your responsibility in the next billing cycle.

Does Paying the Minimum Damage Your Credit History?

The short answer is no. Paying the minimum does not damage your credit history, as long as you make that payment by the due date every billing cycle. Your status with the credit bureau will remain normal. That said, there are other hidden consequences you should be aware of, depending on the situation:

Paying the Minimum on Time

If you consistently pay at least the minimum amount by the due date, your financial institution will report your account status to the credit bureau as normal (not in arrears). Your credit history will remain in good shape. However, while this won't put you on any blacklist, lenders may note that your debt level is rising, which could affect how they assess you if you apply for a larger loan in the future.

If You Miss Payments for Over 90 Days

Problems arise immediately if you can't even manage the minimum payment. Once an account goes unpaid for more than 90 consecutive days, your credit bureau status will be changed to non-performing loan (NPL). This is recorded in the system and seriously damages your creditworthiness - making it impossible to apply for new loans or credit cards with other financial institutions until the debt is fully settled.

The Real Impact of Paying Only the Minimum: What to Know Before You Decide

While paying the minimum won't immediately damage your credit record, the financial consequences that follow are unavoidable. Here's what actually happens when you choose not to pay in full. So you can assess your situation and plan accordingly.

Interest Is Charged Immediately

The moment you pay less than the full amount, your financial institution begins charging interest on the remaining balance straight away. That interest is calculated daily from the date of each transaction - not from your billing cycle cut-off date. This means the longer you carry a balance, the higher the interest charge will be in your next billing cycle.

Your Debt Grows from Compounding Interest

As interest is added to the unpaid principal, your total outstanding balance grows quickly. If you continue paying only the minimum, the money you pay is applied to interest first - leaving very little to reduce the principal. Your debt barely shrinks and the burden keeps growing.

Your Interest-Free Period Is Cancelled

Credit cards typically offer an interest-free period of up to 45–55 days when you pay in full. The moment you pay less than the full amount, this benefit is cancelled immediately. Any new purchases you make after that point will be charged interest from the very first day of the transaction - making your finances more complicated and more expensive to manage.

You Risk Long-Term Debt

Consistently paying only the minimum is the starting point of a long-term debt cycle. With the principal reducing slowly while interest keeps accumulating, it can take years to fully pay off the balance. This ties up money that could otherwise be saved or invested - closing off opportunities to build stability in other areas of your financial life.

KKP Better: A Tool to Help You Manage Your Credit Card Payments

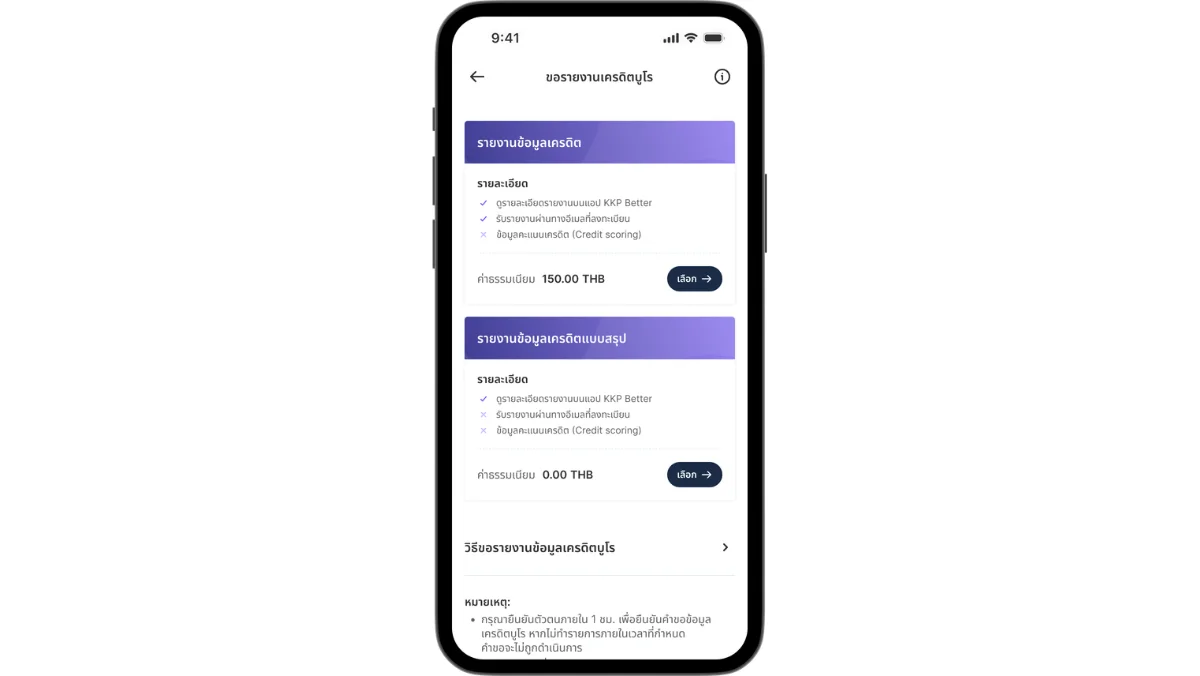

Beyond understanding your debt, keeping track of your account status matters too. KKP Better helps you plan your credit card payments and check your financial history easily. All you need is a savings account with Kiatnakin Phatra Bank. If you don't have one yet, you can open an account online through the app right away. There are 3 credit report options available:

- Summary Credit Report: Provides an overview of the number of accounts, total credit limit and outstanding balance. Suitable for checking your own financial status at a glance. This report cannot be used as a reference with other organisations.

- Full Credit Report: Provides detailed records of loan approvals, payment history, credit card usage and the status of every account you hold with financial institutions that are members of the credit bureau. Suitable for use when applying for a loan.

- Credit Report and Credit Score: Provides in-depth credit information along with your Credit Score, which assesses the likelihood of repayment based on your past history. Suitable for submitting a complete loan application to a financial institution.

Credit Card Minimum Payment FAQ

Final Thoughts

Paying only the minimum on your credit card won't damage your credit history as long as you pay on time. But it comes at the cost of compounding interest that causes your debt to grow and takes far longer to clear. Whenever possible, paying the full amount is always the better choice for your financial health. If you want to manage your finances more effectively, the KKP Better app lets you check your credit bureau status, manage your deposits, and access loan services - all in one place.

Related Products